Embrace NHS APPRENTICESHIP and AVOID UK STUDENT LOAN & LONG-TERM DEBT

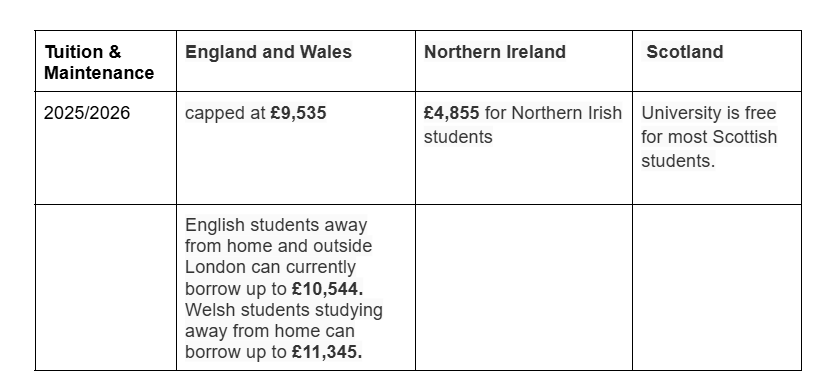

Fifty-three thousand pounds (£53,000) is the average UK graduate debt in 2025, as reported by the House of Commons library. £299,645 stands as the highest individual student debt as reported by the Independent in 2025. Student loans were first introduced in the UK by the conservative government of Margaret Thatcher in the 1990s. It was further developed by her successor, and with it came the student loan companies(SLC). These SLCs are banks in England and Wales that offer and manage these loans to customers, i.e., students. Over the three decades since student loans were introduced, they have undergone several iterations to reach their current state. In summary, they are loans that the UK government lends to someone to enable them to complete higher education at a university or college. It comprises tuition fees paid directly to the educational provider and maintenance costs paid directly to the learner to support their daily upkeep. The UK student loan system is one of the most complex in the developed world for many reasons. I will try to highlight these reasons in this article. First and foremost, tuition fees for UK home students vary across the devolved nations. For the 2025/2026 academic year, as reported by the British Broadcasting Corporation (BBC), below are the rates.

Student Loan & Maintenace rates

The above tuition figures are not inflation-protected, meaning they will rise year by year with overall inflation. The second layer of complexity comes up in how the loans are repaid. But before I address it, it will be prudent to provide more information about UK student loans in general for the lay reader.

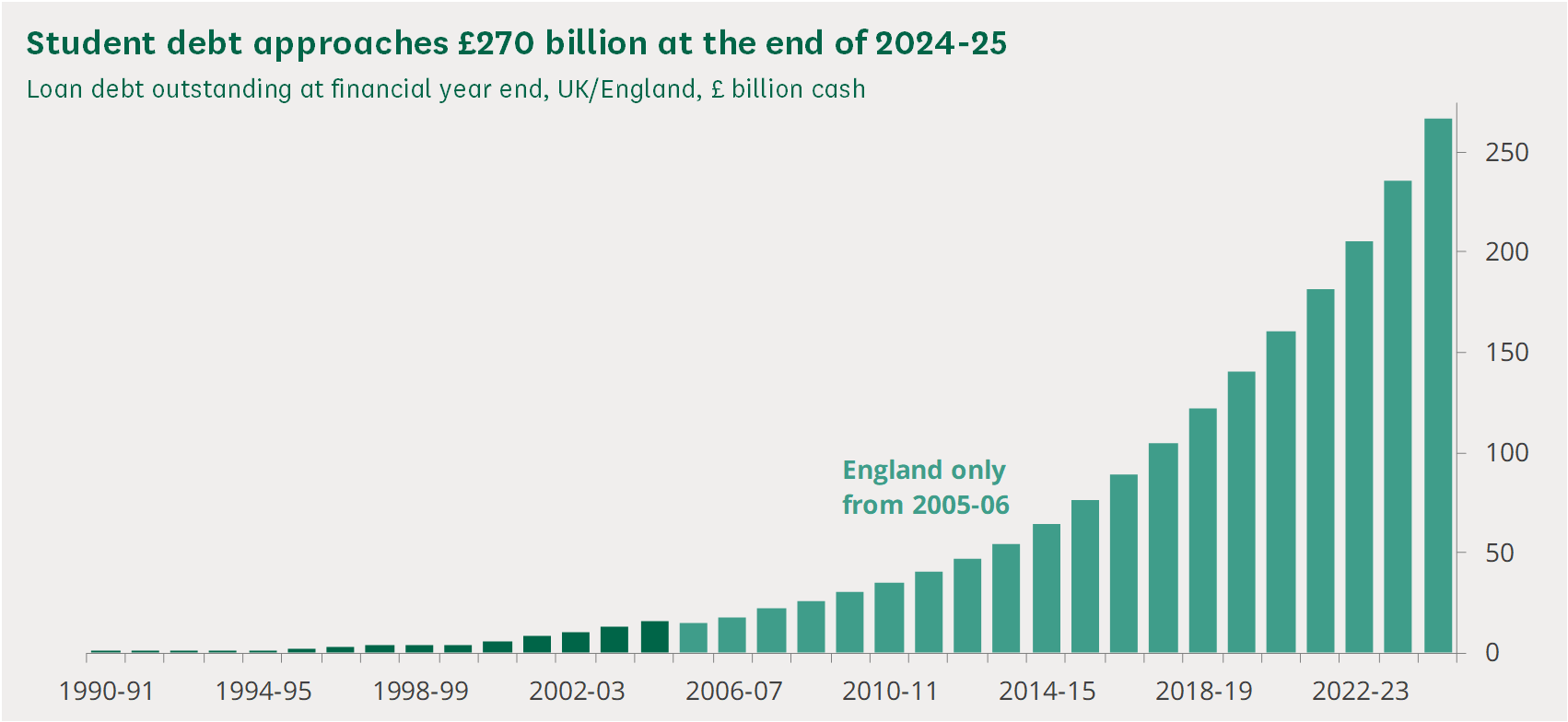

Historically, these loans have had low full repayment compliance, with a forecast of 32% 2022/2023 cohort and 56% for the 2025/2026 cohort. The overall loan budget is huge, standing at an average of £21 billion per year, loaned to around 1.5 million learners. This is about the annual budget of London, a city of about 9 million people. Cumulatively, it has reached £267 billion by March 2025. The total value of UK student loans has reached about £267 billion by March 2025, which is slightly larger than the annual budget of the NHS, estimated at around £180 to £200 billion per year. This means the student loan balance is roughly one and a half times the size of a single year of NHS spending.

In 2022, the OECD published its Education at a Glance, " which reviewed the state of education across several OECD countries. Its findings revealed how England compares to other OECD countries in the following summary: Student loans in England are significantly higher than in other OECD countries. The OECD report shows that students in England borrow over USD 11,900 per year on average, compared with as little as USD 2,900 in some countries. At graduation, average debt in England is around USD 58,500, which is more than double the levels seen in many other OECD countries such as Australia, Canada, and Denmark. Around 94% of students in England graduate with debt, reflecting a system in which over 90% of students rely primarily on loans rather than grants. In contrast, many other countries provide a mix of grants and loans or rely more heavily on public funding. Overall, England combines high tuition fees with a loan-based support system, resulting in the highest levels of student borrowing and graduate debt among OECD countries.

Source: Student Loans Company, Student Loans in England: Financial year 2024-25 (and earlier)

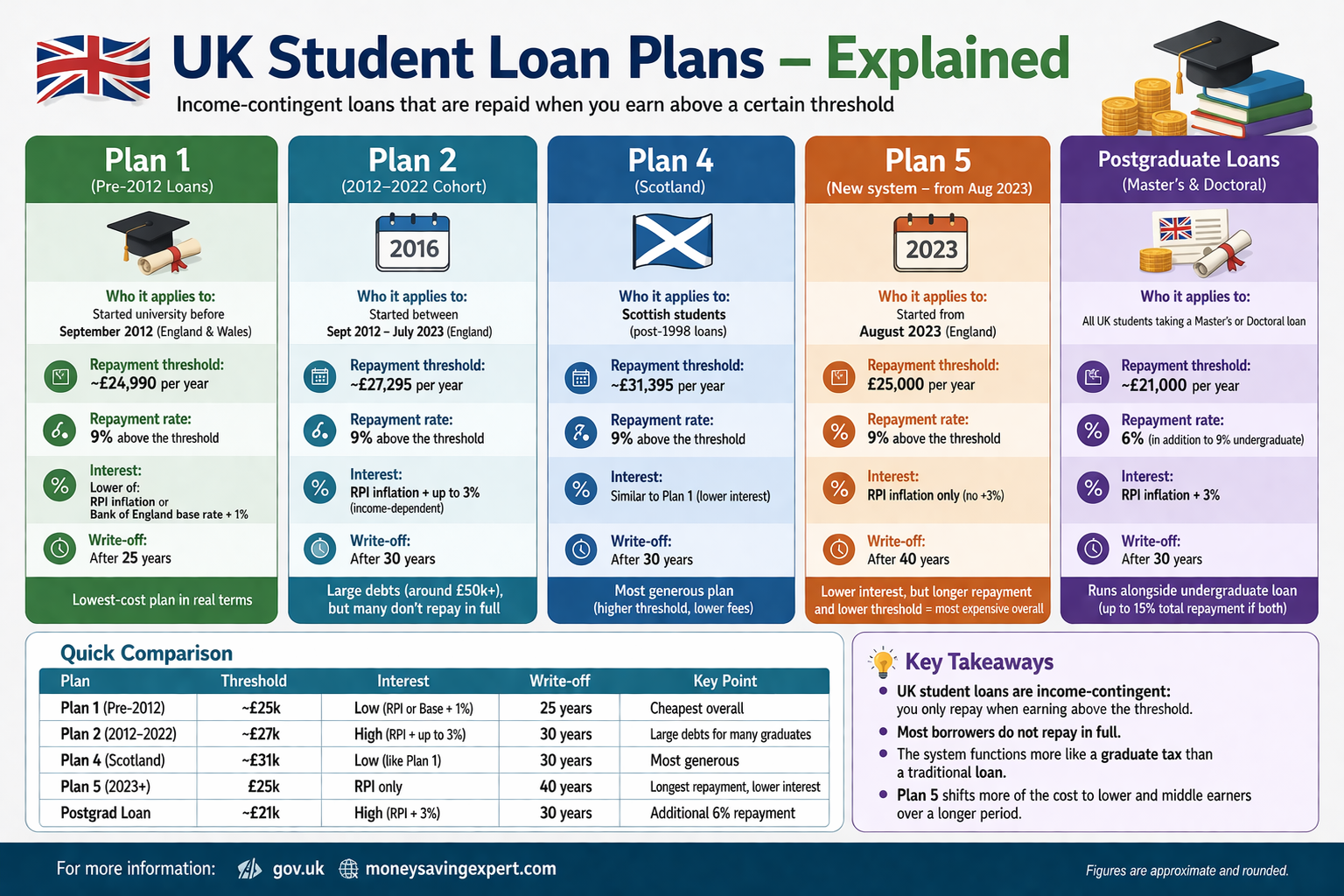

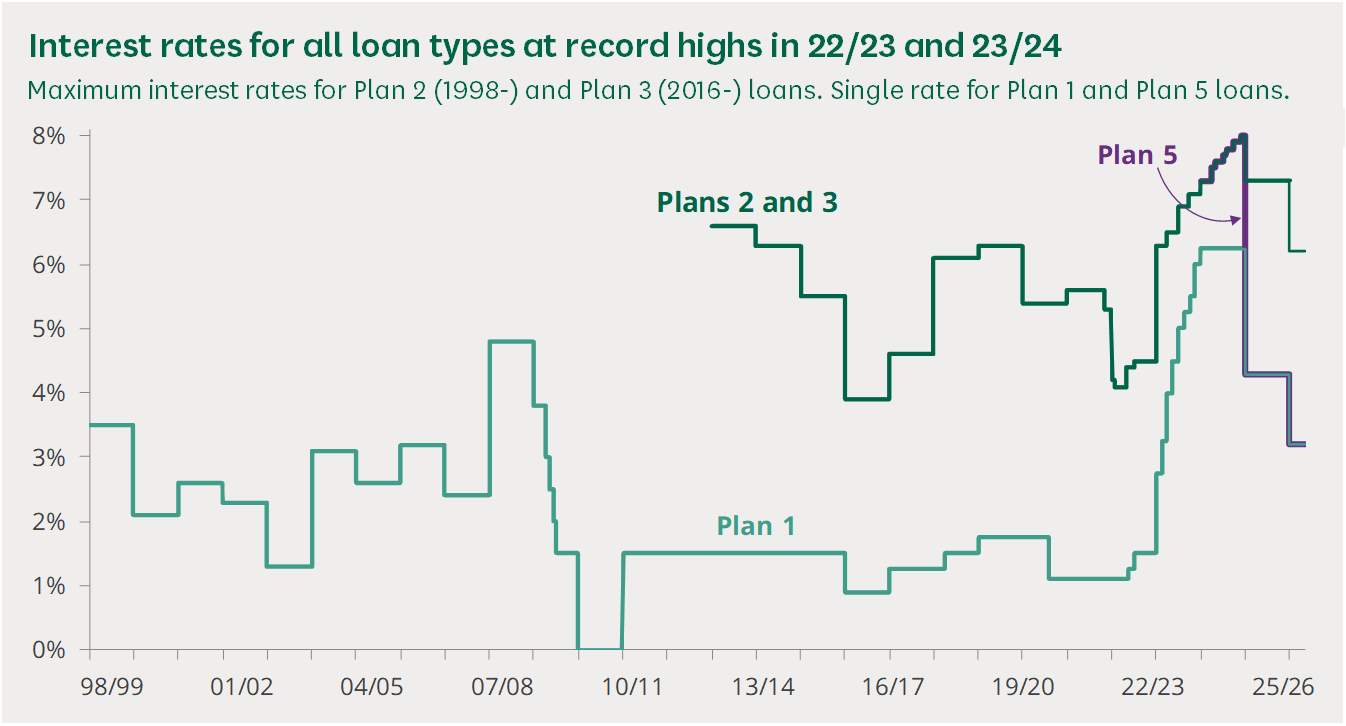

Now, let's look at the repayment plan and the complexity of interest rates and a bit more insight. The maximum interest rate on Plan 2 (post-2012) loans is currently 7.3%. The same rate applies to Plan 3 (postgraduate) loans. The rate on Plan 5 (new undergraduates from 2023/24) loans is lower at 3.2%, the same as for Plan 1 (pre-2012) loans.

UK Student Loan Explained

Student loan Interest rates

Now, how can you, as an education provider, help your students avoid a huge student loan bill by embracing an NHS apprenticeship?

Courses in the various branches of the healthcare tree, medicine, nursing, pharmacy and the allied health degrees tend to take 4-6 years to complete the basic degree. Another 1-3 years if the learner chooses to intercalate a bachelor's or master's degree. It is often expected to have intercalated degrees as they are highly valued, especially in medicine, and improve career prospects and make graduates more competitive in the healthcare job market. As a consequence, university courses in medicine and healthcare are amongst the careers that lead to the most accumulated student loans. Fortunately, the UK government has had a viable alternative that is often ignored, which has been running for years. It was started at the inception of the NHS in 1948 and evolved to its current form of university-based training in the 1990s. It offers the same Education at no cost to the individual and without the need for student loans. One of the options that someone just completing GCSEs can consider if they wish to avoid accumulating student loans is the NHS apprenticeship programme, where the learner has their tuition paid by the NHS in return for in-service training and a salary, completely obviating the need for a study loan. Interestingly, this shortcut is not often presented to education providers in sixth form or colleges to offer to their students as an alternative path.

We at Laj Academy UK have expertise in supporting education providers interested in offering this to their students, navigating the necessary government and NHS compliance, which discourages education providers and their students.

Contact us today

Email: admin@lajacademy.co.uk

Call:07787720164

Fill a form, and we will call you back